Franchising has become an increasingly popular business model, offering individuals the opportunity to own and operate their own businesses with the support of an established brand. As a broker, it’s crucial to have a comprehensive understanding of franchise agreements in order to guide your clients through the process effectively. In this guide, we will delve into the intricacies of franchise agreements, exploring their key components, legal considerations, negotiation strategies, and more.

What is a Franchise Agreement?

A franchise agreement is a legally binding contract between a franchisor (the owner of the established brand) and a franchisee (the individual or entity interested in purchasing the right to operate a franchise). It outlines the terms and conditions under which the franchisee will operate the business.

Including:

- Use of the franchisor’s trademarks

- Payment of fees

- Provision of support and training

Understanding the nuances of these agreements is vital for brokers to assist their clients throughout the franchise acquisition process.

One important aspect of a franchise agreement is the duration of the contract. Typically, franchise agreements have a fixed term, which can range from a few years to several decades. The length of the contract can have significant implications for both the franchisor and the franchisee, as it determines the length of time the franchisee will have the right to operate the business and the level of commitment required from both parties.

In addition to the terms and conditions, franchise agreements often include provisions related to territorial rights. These provisions define the geographic area in which the franchisee has the exclusive right to operate the franchise. This helps protect the franchisee from competition within their designated territory and ensures that they have a viable market to operate their business.

They may also include provisions for territorial expansion, allowing the franchisee to open additional locations within their territory or in new territories as they grow their business.

The Role of Brokers in Franchise Agreements

As a broker, your role in franchise agreements is to act as an intermediary between the franchisor and franchisee, guiding your clients through the complex world of business ownership. You provide expertise and guidance to help potential franchisees evaluate the risks and rewards of various franchise opportunities. Brokers can also assist in negotiating favorable terms and conditions for their clients, ensuring that both parties’ interests are protected.

In addition to guiding potential franchisees through the evaluation process, brokers also play a crucial role in assisting with the initial setup of the franchise. This includes helping franchisees navigate the legal and regulatory requirements, such as obtaining necessary licenses and permits. Brokers can also provide valuable insights into the local market, helping franchisees choose the most suitable location for their business.

Furthermore, brokers often have access to a network of industry professionals.

Examples:

- Lawyers

- Accountants

- Marketing experts

This network can be instrumental in ensuring that franchisees have the necessary support and resources to successfully launch and operate their franchise.

Key Components of a Franchise Agreement

A franchise agreement typically consists of various components that lay the foundation for the franchisor-franchisee relationship.

These may include:

- Franchise fee

- Royalty payments

- Territory rights

- Operational guidelines

- Marketing requirements

- Termination clauses

Understanding each of these components in detail allows brokers to provide valuable insights to their clients during the decision-making process.

One important component of a franchise agreement is the franchise fee. This is the initial payment made by the franchisee to the franchisor in exchange for the right to operate a franchise. It often covers the costs of training, support, and the use of the franchisor’s brand and intellectual property. It is important for franchisees to understand the amount and payment terms of the franchise fee before entering into an agreement.

Exploring Different Types of Franchise Agreements

Franchise agreements come in various forms, each with its own set of rights and obligations. It is crucial for brokers to educate themselves on the different types of franchise agreements:

- Single unit franchises

- Multi-unit franchises

- Area development agreements

-

Master franchises

By understanding the nuances and advantages of each type, brokers can better match their clients’ needs with the suitable franchise opportunities available.

Single unit franchises are the most common type of franchise agreement. In this arrangement, the franchisee operates a single location of the franchised business. This type of agreement is ideal for individuals who are new to franchising or prefer to focus on one location at a time.

On the other hand, multi-unit franchises allow franchisees to operate multiple locations of the same franchised business. This type of agreement is suitable for experienced franchisees who have the resources and capacity to manage multiple units simultaneously. It offers economies of scale and the potential for greater profitability.

Legal Considerations in Franchise Agreements

Franchise agreements are legally binding documents that must comply with both federal and state laws. Brokers need to be aware of the legal considerations involved in franchise agreements.

Including:

- Franchise disclosure requirements

- Non-compete clauses

- Intellectual property protection

- Dispute resolution mechanisms

Working with legal professionals, brokers can ensure that their clients enter into agreements that fully comply with the relevant legal framework.

One important legal consideration in franchise agreements is the requirement for franchise disclosure. Franchisors are typically required to provide potential franchisees with a Franchise Disclosure Document (FDD) that contains detailed information about the franchise opportunity.

This document includes information about:

- Franchisor’s background

- Franchise system

- Initial investment required

- Ongoing fees

- Other important details

Brokers must ensure that their clients receive and review the FDD before entering into any franchise agreement.

Another legal consideration in franchise agreements is the inclusion of non-compete clauses. These clauses restrict franchisees from operating a similar business within a certain geographic area for a specified period of time. They are designed to protect the franchisor’s brand and prevent competition from within the system. Brokers should carefully review and negotiate the terms of non-compete clauses to ensure that they are fair and reasonable for their clients.

How to Negotiate a Favorable Franchise Agreement for Your Clients

Negotiating a favorable franchise agreement is crucial for the long-term success of the franchisee. Brokers play a vital role in advocating for their clients during the negotiation process.

This includes discussing factors such as:

- Initial investment

- Royalty rates

- Advertising and marketing fees

- Territory exclusivity

- Renewal terms

Understanding the needs and goals of both parties, brokers can facilitate a mutually beneficial outcome.

One important aspect to consider when negotiating a franchise agreement is the length of the contract. Franchisees should aim for a contract term that provides enough time to recoup their initial investment and generate a profit. Additionally, it is essential to negotiate favorable renewal terms that allow for potential expansion or relocation of the franchise.

Another key factor to address during negotiations is the level of support and training provided by the franchisor. Franchisees should seek agreements that outline comprehensive training programs, ongoing support, and access to resources such as marketing materials and operational guidance. This ensures that franchisees have the necessary tools and knowledge to successfully operate their business.

Common Challenges in Franchise Agreements and How to Overcome Them

Franchise agreements can present challenges for both franchisors and franchisees. Brokers must be aware of these potential challenges.

Examples:

- Financial projections

- Operational restrictions

- Changes in market conditions

-

Exit strategies

Anticipating these challenges and fostering open communication between all parties, brokers can assist their clients in navigating and overcoming potential obstacles.

Important Clauses to Look for in a Franchise Agreement

Franchise agreements contain numerous clauses that impact the rights and responsibilities of both franchisors and franchisees. Brokers should carefully review these clauses, ensuring that they address critical aspects such as:

- Training and support

- Advertising and marketing

- Sale of the franchise

- Transferability of the agreement

- Renewal terms

Evaluating these clauses ensures that brokers provide their clients with a clear understanding of the obligations they will undertake as franchisees.

Understanding the Financial Obligations in a Franchise Agreement

Financial considerations are integral to franchise agreements. Brokers must help their clients fully understand the financial obligations they will incur throughout the agreement’s duration.

This includes:

- Initial franchise fee

- Royalty payments

- Advertising and marketing fees

- Any additional charges

Thoroughly evaluating the financial aspects and discussing them transparently, brokers can assist their clients in making informed decisions.

Assessing the Rights and Responsibilities of Franchisees and Franchisors

Franchise agreements establish the rights and responsibilities of both franchisors and franchisees. Brokers should assist their clients in understanding these roles.

Including:

- Use of intellectual property

- Product sourcing

- Operational support

- Quality control

-

Reporting requirements

Ensuring clarity on these aspects, brokers help their clients enter into franchise agreements with a full understanding of the expectations and obligations involved.

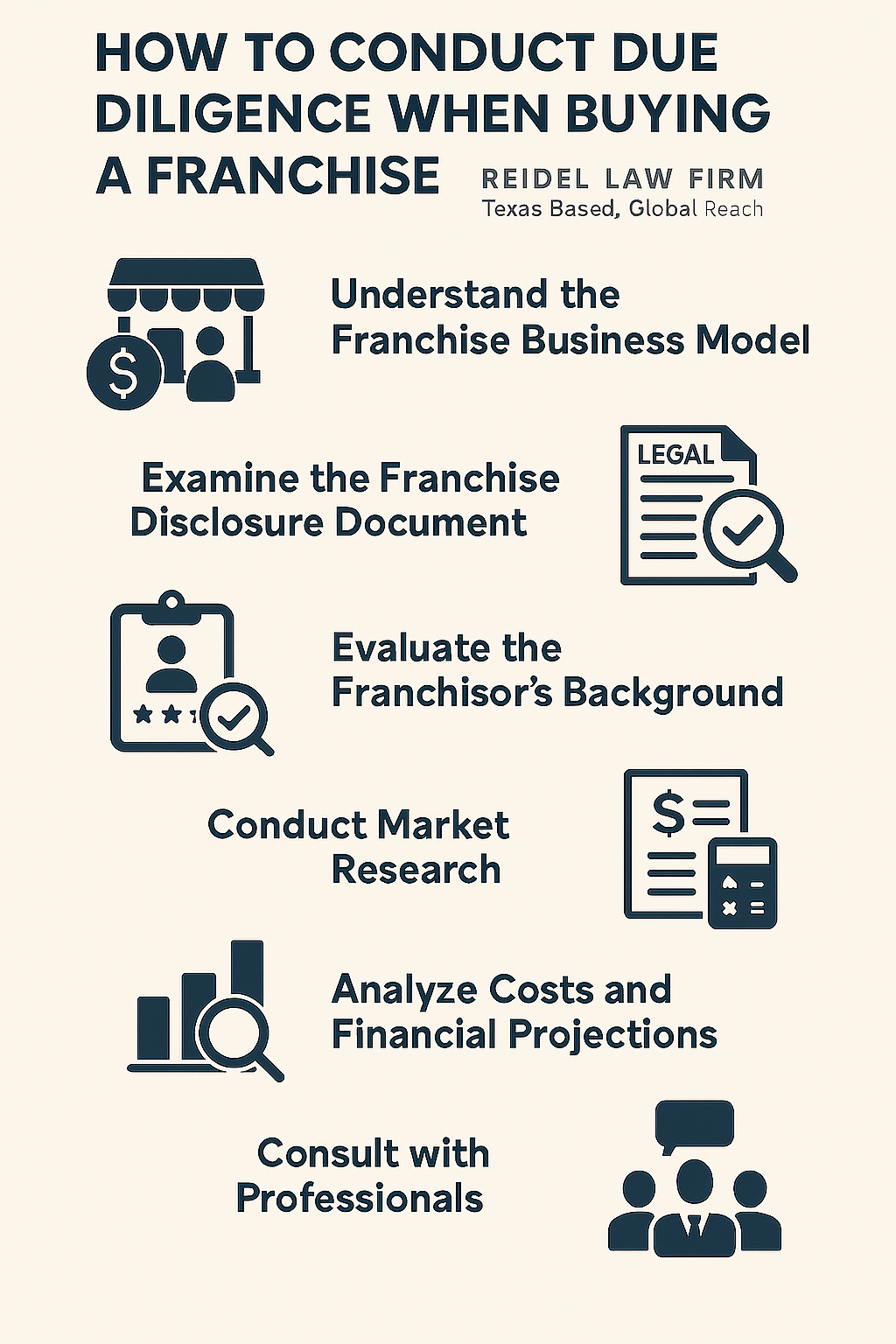

The Importance of Due Diligence in Evaluating Franchise Agreements

Conducting due diligence is critical before entering into any franchise agreement. Brokers should guide their clients through this process, which involves researching:

- Franchisor’s background

- Financial health

- Litigation history

- Reputation within the industry

Performing thorough due diligence, brokers assist their clients in making informed decisions and minimize the risks associated with investing in a franchise opportunity.

How to Evaluate the Profit Potential of a Franchise Agreement

The profit potential of a franchise is a fundamental consideration for potential franchisees. Brokers should work closely with their clients to evaluate the financial projections provided by franchisors, analyzing factors such as:

- Initial investment

- Revenue streams

- Operational costs

-

Market demand

Conducting a comprehensive evaluation, brokers can provide valuable insights to their clients and help them determine the potential return on investment.

Exploring the Training and Support Provided in Franchise Agreements

Franchise agreements often include provisions for training and ongoing support. Brokers should investigate the training programs, operational manuals, and other resources offered by franchisors. Understanding the level of training and support provided, brokers can help their clients assess the franchisor’s commitment to the success of its franchisees and guide them towards opportunities that offer comprehensive training and ongoing support.

Tips for Marketing and Promoting Franchise Opportunities to Potential Buyers

Finally, brokers play a pivotal role in marketing and promoting franchise opportunities to potential buyers. By leveraging their network and industry knowledge, brokers can identify potential franchisees who may be interested in specific opportunities. Furthermore, brokers should assist franchisors in developing effective marketing strategies and materials to attract qualified individuals who align with the franchisor’s vision and requirements.

As a broker, mastering the nuances of franchise agreements is essential for effectively guiding your clients through the franchise acquisition process. Understanding the various components, legal considerations, negotiation strategies, and potential challenges allows you to provide valuable insights and optimize outcomes for both franchisors and franchisees. By educating yourself on these topics and staying abreast of industry developments, you position yourself as a trusted advisor in the exciting world of franchising.

Reidel Law Firm Franchise Broker Services

As experts in franchise law, we can help your franchisee clients with FDD reviews.

In addition, our legal team can advise on ways to shore up gaps in the following areas:

- Review personal guaranty and real estate control docs

- Franchisee formation, guidance, and asset protection

- Franchise operating compliance audit and coaching

By effectively managing risk and maximizing opportunities for businesses we answer the needs of our clients wherever and whenever they arise.

Call Reidel Law Firm today at (832) 510-3292 or fill out our contact form. And see how our advice can provide a solid foundation for your brokerage.